Many moons ago I walked into my first job interview and seated myself across the CEO of the company. This is how the interview went:

CEO: Do you know how to type?

Me: No. (I grew up without a computer in the house!)

CEO: Come back when you know how to type.

He then handed me a “Mavis Beacon Teaches Typing” disc and wished me a good day.

P.S. For the next 48 hours I was glued to my chair practicing typing. Two days later I returned the disc (and got the job!).

I am tremendously grateful to this CEO for forcing me to learn how to type correctly. When I start my day and find 100+ emails in my inbox, I can respond quickly and professionally without wasting all morning pecking away at the keyboard.

Today, employing a large staff who perform various computer tasks all day, I stress the importance of making sure every member of my team can type quickly and correctly.

The ROI is simple. Take for example a team of 10 employees earning $15 per hour and typing at 25 words per minute:

This is probably one of the simplest and fastest investments you can make with your staff. It takes 2 – 3 days to learn how to type and they will practice and get faster as they go about their daily tasks.

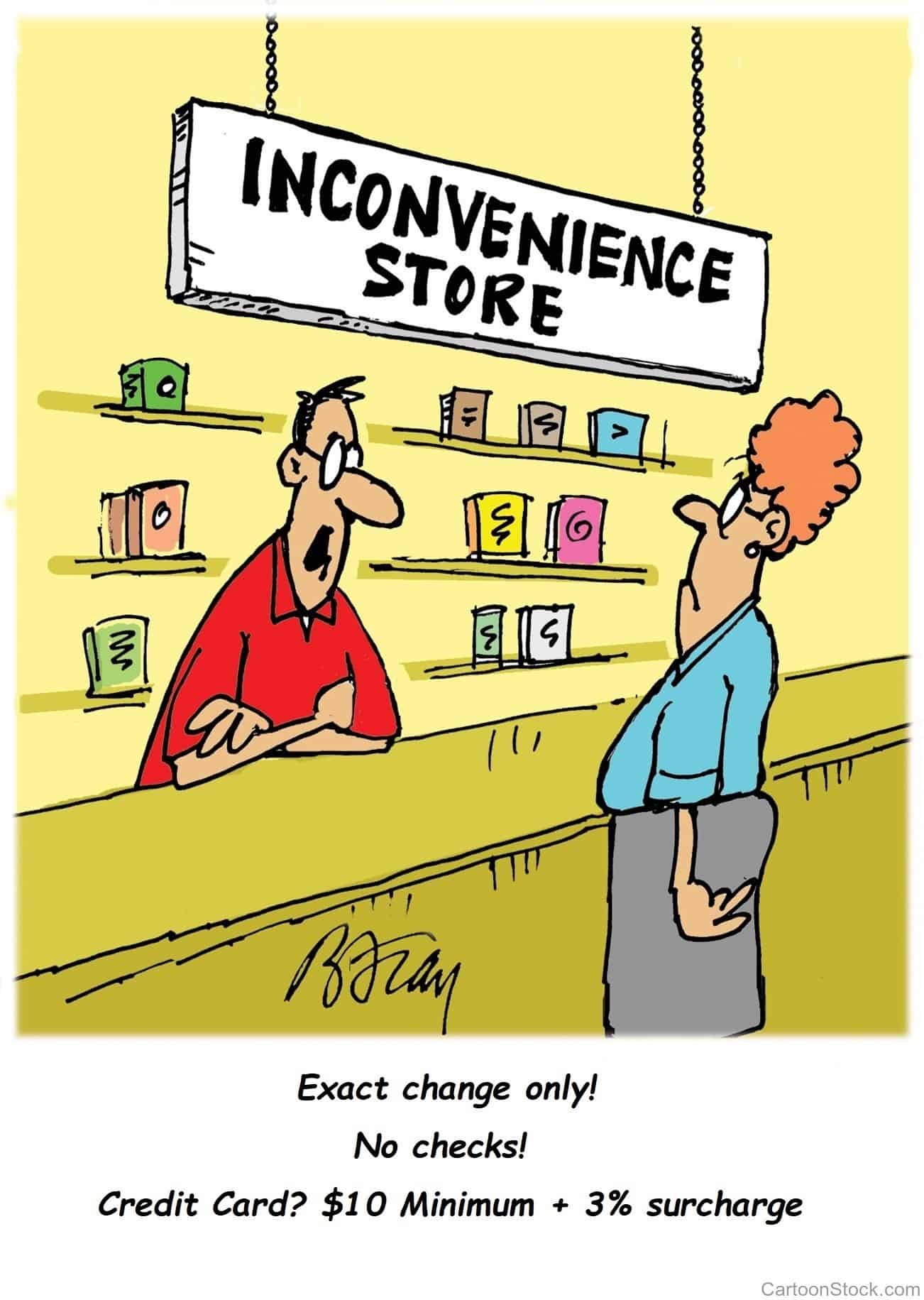

You’re about to give your credit card to make a payment when the merchant says, “Credit card transactions are an extra 3%.”

This is called a credit card surcharge. Though it’s annoying, there’s a reason merchants add it: to cover their costs. You’ll rarely see surcharges at large retailers. But you could see them at mom-and-pop establishments, where bottom lines are more sensitive to credit card processing fees. Is it legal for the merchant to charge you an extra surcharge?

In most States, merchants aren’t barred by law from adding surcharges. According to the Durbin Amendment of the Dodd–Frank Act, retailers are allowed to add a surcharge on credit card transactions. (They are not allowed to add surcharges on debit card or prepaid card transactions.)

Merchants are also allowed to require minimum purchases for credit card purchases — up to $10.

However, Surcharges are illegal across the board in these 9 states:

Colorado

Connecticut

Florida

Kansas

Maine

Massachusetts

New York

Oklahoma

Texas

Does it make sense for you to pay an extra 3% to use your credit card?

That really depends on why you wish to use your credit card in the first place. If it’s simply for convenience, it might not make sense for you to pay an extra 3% for this convenience. However if you need the 30 – 45 day cash float that your credit card afford you, then it might be the only way you can make the purchase. Additionally, some savvy business owners may have a credit card that earns them 2% cash back and the cash back money is tax free (grey area…Speak to your Accountant.). If you’re in a high tax bracket, it may be well worth it to pay 3% and get back 2% of that tax free.

Does it make sense for business owners to pass on the fee?

It really comes down to your customers. If you implement a surcharge, it comes at the risk of losing customers who are put off by additional charges for credit card.

When consumers were asked would they pay extra to use a credit card at a business, 64% said they wouldn’t pay an extra fee. Additionally, credit cards have become a standard method of payment in virtually every industry and every large corporation accepts credit cards without surcharging.

Finally, if your fees are too high, it might be time to look for a new processor. If you’re already a Banquest client, let us know how we can help you when it comes to surcharges. If you’re not a client but interested in how we can support your business, click here to contact us today!

It’s our mission to reduce the costs and headaches associated with credit card processing, so we’d be honored to earn your business. Happy Tuesday & Happy Selling! Kevin

I debated with myself before writing this blog: is it really necessary? Is there anyone out there that doesn’t already know this information?

Unfortunately we and our colleagues in the payment processing industry deal with this all the time. My staff, who unfortunately has to clean up these messes, insist that many of the abusers are truly innocent. They simply don’t know that what they are doing is wrong.

What I am referring to is the practice of charging or swiping ones own credit card to their own business – as a quick way to get funds into their bank account. (i.e. a business owner is short $20,000 for payroll, so he swipes his own credit card for $20,000 and has the funds in his account the next day! Sometimes there may even be legitimate reasons for doing so such as when someone owns multiple businesses and he is using his card from business A to pay business B.)

I’m not here to discuss whether or not this is a financially good idea in terms of the % rate… (It’s not!)

The credit card processors strictly prohibit such transactions and will terminate any account that processes such a transaction. They’re pretty good about catching them too. Sometimes the processor will place the merchant on a blacklist that is shared with all US processors ensuring that this business will never get approved for a merchant account anywhere.

In short: never charge your own (or your family or business partners) credit card to your own merchant account.

Yesterday a good friend (and client) and I celebrated the 3 year anniversary of the day he came to the realization his business was a complete failure!

You see, my friend had a successful printing business for many years. A combination of a slowdown in sales, excessive personal spending, and the dream to be one of the ‘big boys’ which led him to finance expensive printing equipment, had him running around trying to catch his tail. He started borrowing heavily from friends and family. When that dried up, he charged his own credit cards to his business (a huge no-no!) to be able to cover his payroll expenses. He was deep in the mud and couldn’t see a way out.

A dedicated caring employee suggested they bring in an outsider with business experience to do a real assessment of the situation.

Some very tough measures had to be taken. For starters he had to sit down with his wife and share with her their true financial situation. He gave up his luxury cars, vacations, and put a complete stop to online (impulsive) shopping.

He reached out to all his creditors and humiliatingly admitted the truth and asked for time and terms to slowly pay back.

They focused on what his core strengths were and soon realized that his business model of doing all the printing in-house was actually costing him more than brokering out the jobs. He laid off most of his staff and restructured his business as a full-service business (graphics, design, printing) while brokering out the actual printing.

Thankfully, he was able to repay most of his old debt and is continuing to do so. He has rebuilt his company and reputation, and is able to look back and see the good in what once looked like a very bleak situation.

There is a lot to be learned from his experiences, but here are the 2 points that are really important:

Sometimes it takes an outsider to assess your business. A business owner may be stuck in the box and cannot see what others might see.

While giving up is not a virtue, sometimes you need to abort and take a new path.